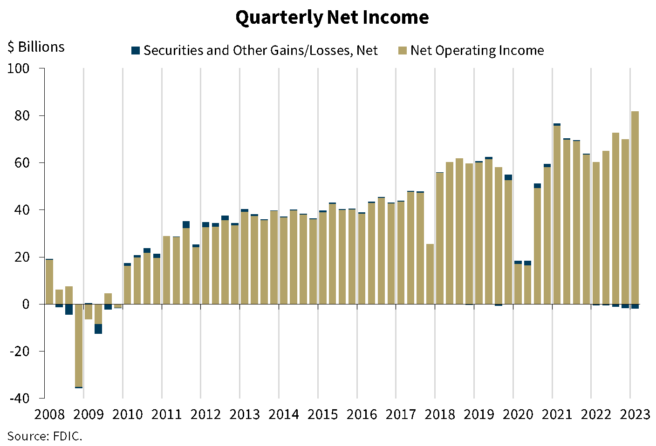

On May 31, the Federal Deposit Insurance Corporation (FDIC) released its First Quarter 2023 Quarterly Banking Profile showing a first quarter aggregate net income of $79.8 billion for its 4,672 insured commercial banks and savings institutions, an increase of $11.5 billion from fourth quarter 2022. In a statement accompanying the release of the Profile, FDIC Chairman Martin Gruenberg stated: “Despite the recent period of stress, the banking industry has proven to be quite resilient. Net income still remains high by historical measures even after deducting one-time transactions, asset quality metrics are favorable, and the industry remains well capitalized.” Chairman Gruenberg did acknowledge, however, that these results include only a few weeks of the banking stress that began in early March. The more lasting effects of recent bank failures may not be fully apparent until after the second quarter.

Highlights from the Profile include:

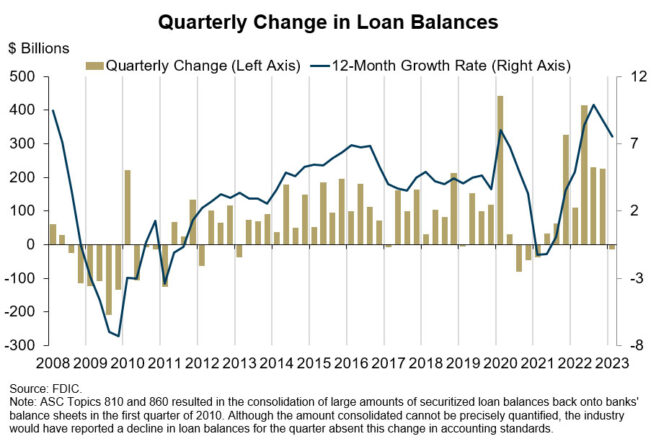

- Growth in noninterest income, reflecting the acquisition of two failed institutions and record-high trading revenue at large banks, outpaced lower net interest income and higher noninterest expense.

- Quarterly net income for the 4,230 community banks insured by the FDIC declined by $306.0 million (4.2%). However, community bank net income improved relative to a year ago.

- Asset quality remained favorable as loans that were 90 days or more past due or on nonaccrual status increased by only 0.75%.

- The Deposit Insurance Fund (DIF) balance was $116.1 billion, down $12.1 billion from the end of fourth quarter 2022.

Despite the net growth, Chairman Gruenberg cautioned that, “[t]he banking industry continues to face significant downside risks from the effects of inflation, rising market interest rates, slower economic growth, and geopolitical uncertainty. Credit quality and profitability may weaken due to these risks and may result in a further tightening of loan underwriting, slower loan growth, higher provision expenses, and liquidity constraints. Commercial real estate portfolios, particularly loans backed by office properties, face challenges should demand for office space remain weak and property values continue to soften.”

In that vein, the Profile noted two key trends. First, there have been marked quarter-over-quarter changes in the banking industry’s yield on loans and cost of deposits – i.e., yields on loans increased by 32 basis points while the cost of deposits increased by 43 basis points, which helps to explain the recent tightening of net interest margin. The FDIC’s historical experience suggests that the gap between changes in loan yields and deposit costs tends to increase early in rate-rising cycles but then decreases and often reverses when market rates stabilize or decline.

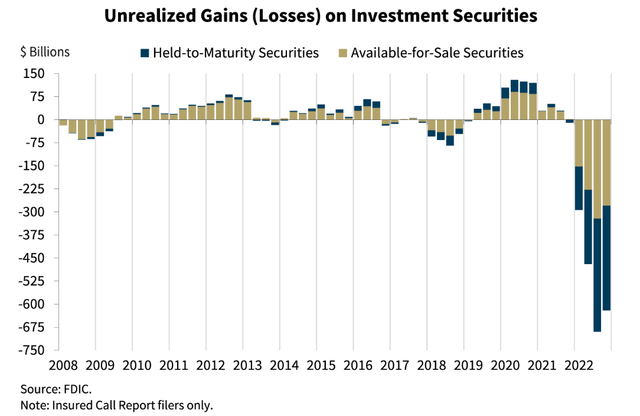

Further, since the beginning of 2022, there has been an elevated level of unrealized losses on investment securities due to the increases in market interest rates. Unrealized losses on available-for-sale and held-to-maturity securities totaled $515.5 billion in the first quarter, down 16.5 percent from the prior quarter, primarily due to declines in medium- and long-term interest rates.

These will be matters of ongoing supervisory attention by the FDIC. In particular, the FDIC has pledged to closely monitor liquidity and access to funding across the banking industry.